The diplomatic progress that had been quietly driving oil prices lower since April evaporated on June 1. Iran’s Foreign Minister Abbas Araghchi announced that Tehran was suspending all ceasefire negotiations with the United States, citing Israeli strikes on targets in Lebanon as justification. The same day, Iran renewed its threat to close the Strait of Hormuz entirely. Oil jumped more than 7% in a single session. Brent crude climbed back above $100 a barrel. And for Europe, already approaching summer with gas storage at its lowest in years, the timing is about as bad as it gets.

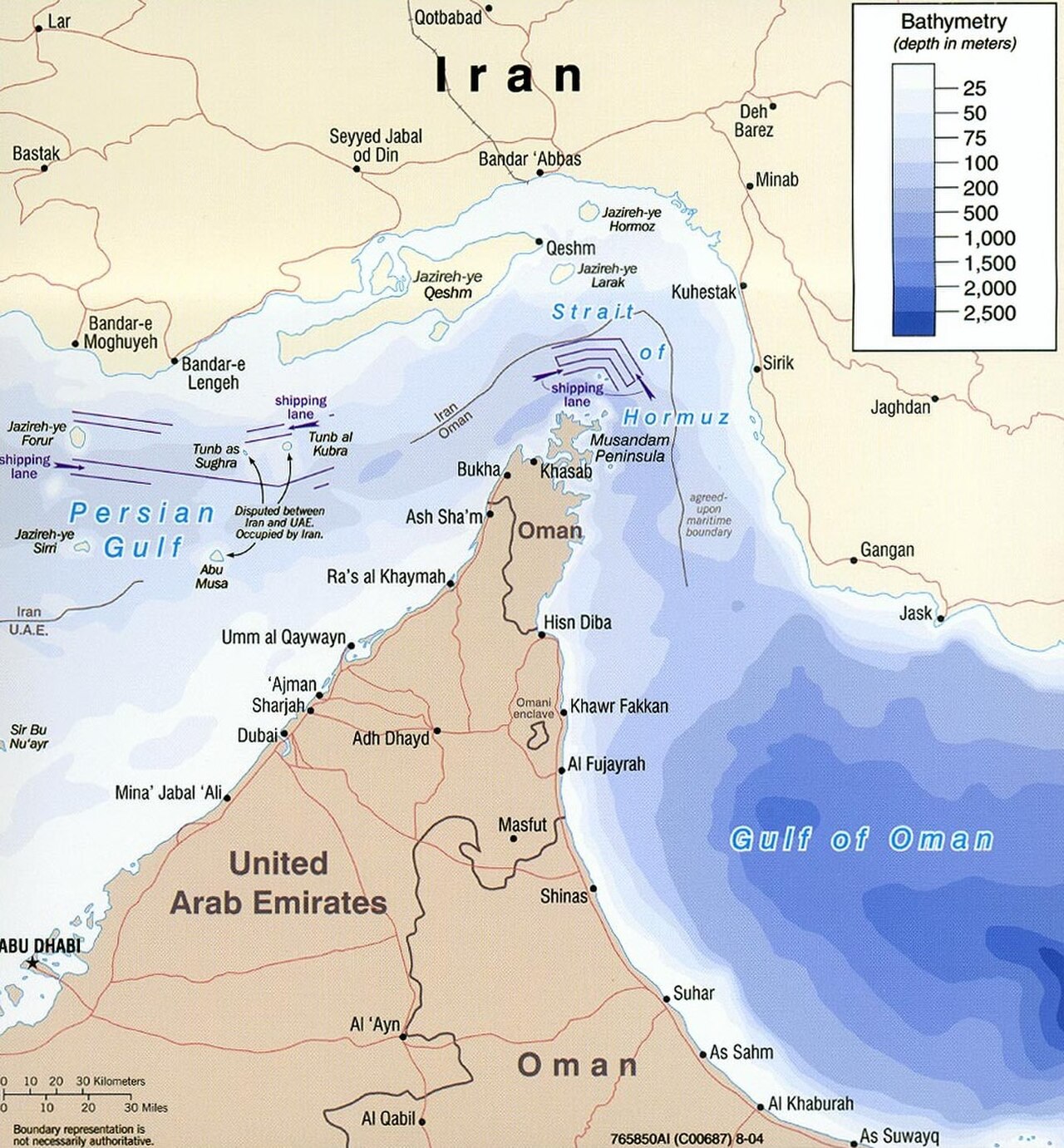

Europe’s vulnerability to a Hormuz crisis is structural. The continent replaced Russian pipeline gas after the 2022 invasion by pivoting heavily to Qatari LNG — and Qatar routes approximately 80% of its LNG exports through the Strait of Hormuz. There is no ready substitute at scale. Norwegian volumes cannot bridge the gap. US LNG is a partial replacement, but at a higher price point, over longer supply chains, and with no guaranteed political commitment to prioritise European customers over Asia-Pacific buyers.

EU gas storage now stands at around 30%, a level that analysts describe as critically low for the start of the summer refill season. To reach the roughly 90% target required before winter, Europe must spend the next five months aggressively rebuilding reserves — at a moment when the cost of doing so has just risen sharply. Dutch TTF gas futures, the European benchmark, have climbed to around €60 per megawatt hour. ACER estimates the additional weekly energy import bill at €2 to €3 billion if the disruption is sustained.

The European Central Bank, which had been preparing the ground for summer rate cuts, has already revised growth forecasts downward in response to the energy volatility. A prolonged second energy shock — on top of the one already absorbed between 2022 and 2024 — would complicate the Bank’s calculus significantly. For households and businesses still carrying the residual cost of the previous cycle, a fresh surge in energy bills is not an abstraction.

Europe’s immediate problem is that it has no meaningful leverage over the one variable that matters: whether Iran and the United States reach a deal, and how fast. Writing in the Financial Times, analysis described the prospect of rapid Hormuz reopening as “bleak” — pointing to deep mutual distrust, the fragility of any arrangement that depends on sustained Israeli military restraint, and the difficulty of reaching durable terms through the back-channel mediators both sides are using.

Trump’s claim that a deal was reachable “over the next week” generated limited confidence in financial markets, which have grown accustomed to pricing the distance between his public statements and actual diplomatic outcomes. The ceasefire process involves multiple layers of intermediary engagement, and the triggering incident — Israeli strikes in Lebanon — introduces variables Washington does not fully control.

The Commission has not yet formally invoked the METSAF framework — the state aid flexibility mechanism first deployed during the 2022 crisis that allows member states to subsidise energy costs without triggering standard state aid rules. That framework is still in place and could be activated relatively quickly. Energy officials are understood to be reviewing contingency procurement options, though public communications remain in monitoring mode.

Europe replaced one energy dependency with another. The pipeline-to-LNG pivot of 2022 reduced Russian leverage, but it transferred European exposure to a supply route running through one of the world’s most geopolitically volatile chokepoints. The 30% storage figure is not just a logistical data point. It is the margin of error Europe has left if diplomacy stalls and the Hormuz disruption extends across the summer. At this point in the year, that margin is thin.

.png)